statsmodels.tsa.filters.bk_filter.bkfilter¶

-

statsmodels.tsa.filters.bk_filter.bkfilter(x, low=

6, high=32, K=12)[source]¶ 使用Baxter-King带通滤波器过滤时间序列。

- Parameters:¶

- xarray_like

一个1维或2维的ndarray。如果是2维的,变量假设在列中。

- low

float 振荡的最小周期,即Baxter和King建议,Burns-Mitchell美国经济周期对于季度数据为6,对于年度数据为1.5。

- high

float BK建议的最大周期表明,美国商业周期对于季度数据为32,对于年度数据为8。

- K

int 滤波器的领先滞后长度。Baxter和King建议对于季度数据截断长度为12,对于年度数据截断长度为3。

- Returns:¶

ndarrayx的周期性成分。

另请参阅

statsmodels.tsa.filters.cf_filter.cffilterChristiano Fitzgerald 非对称随机游走滤波器。

statsmodels.tsa.filters.bk_filter.hpfilterHodrick-Prescott 滤波器。

statsmodels.tsa.seasonal.seasonal_decompose使用移动平均法分解时间序列。

statsmodels.tsa.seasonal.STL使用LOESS进行季节趋势分解。

注释

返回原始序列的居中加权移动平均值。其中权重 a[j] 是计算得出的

a[j] = b[j] + theta, for j = 0, +/-1, +/-2, ... +/- K b[0] = (omega_2 - omega_1)/pi b[j] = 1/(pi*j)(sin(omega_2*j)-sin(omega_1*j), for j = +/-1, +/-2,...并且 theta 是一个归一化常数

theta = -sum(b)/(2K+1)请参阅笔记本 时间序列过滤器 以获取概述。

参考文献

- Baxter, M. and R. G. King. “Measuring Business Cycles: Approximate

带通滤波器用于经济时间序列。” 经济学与统计学评论,1999年,81(4),575-593。

示例

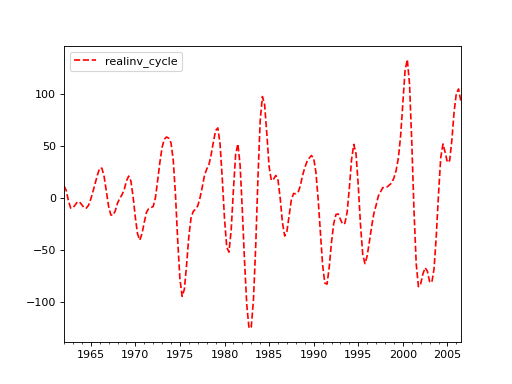

>>> import statsmodels.api as sm >>> import pandas as pd >>> dta = sm.datasets.macrodata.load_pandas().data >>> index = pd.DatetimeIndex(start='1959Q1', end='2009Q4', freq='Q') >>> dta.set_index(index, inplace=True)>>> cycles = sm.tsa.filters.bkfilter(dta[['realinv']], 6, 24, 12)>>> import matplotlib.pyplot as plt >>> fig, ax = plt.subplots() >>> cycles.plot(ax=ax, style=['r--', 'b-']) >>> plt.show()

{kind=link}

{kind=link}

Last update:

Oct 16, 2024