statsmodels.tsa.filters.cf_filter.cffilter¶

-

statsmodels.tsa.filters.cf_filter.cffilter(x, low=

6, high=32, drift=True)[source]¶ 克里斯蒂亚诺·菲茨杰拉德不对称,随机游走滤波器。

- Parameters:¶

- xarray_like

要过滤的1维或2维数组。如果是2维,则假设变量在列中。

- low

float 最小振荡周期。低于低周期的特征将被过滤掉。默认值为6(对于季度数据),对应1.5年的周期。

- high

float 振荡的最大周期。高于高周期的特征将被过滤掉。默认值为32(对于季度数据),对应于8年的周期。

- driftbool

是否从数据中去除趋势。趋势估计为 np.arange(nobs)*(x[-1] - x[0])/(len(x)-1)。

- Returns:¶

- cyclearray_like

x在周期性低和高之间的特征。

- trendarray_like

去除周期后的数据趋势。

另请参阅

statsmodels.tsa.filters.bk_filter.bkfilterBaxter-King 滤波器。

statsmodels.tsa.filters.bk_filter.hpfilterHodrick-Prescott 滤波器。

statsmodels.tsa.seasonal.seasonal_decompose使用移动平均法分解时间序列。

statsmodels.tsa.seasonal.STL使用LOESS进行季节趋势分解。

注释

请参阅笔记本 时间序列过滤器 以获取概述。

示例

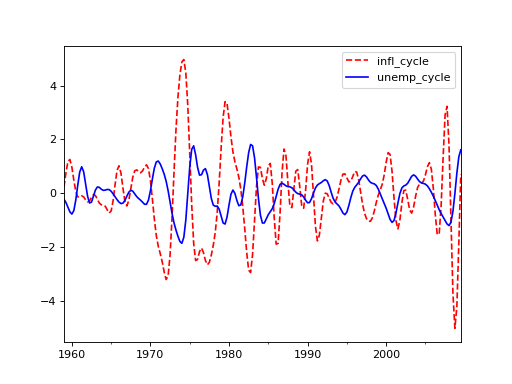

>>> import statsmodels.api as sm >>> import pandas as pd >>> dta = sm.datasets.macrodata.load_pandas().data >>> index = pd.DatetimeIndex(start='1959Q1', end='2009Q4', freq='Q') >>> dta.set_index(index, inplace=True)>>> cf_cycles, cf_trend = sm.tsa.filters.cffilter(dta[["infl", "unemp"]])>>> import matplotlib.pyplot as plt >>> fig, ax = plt.subplots() >>> cf_cycles.plot(ax=ax, style=['r--', 'b-']) >>> plt.show()

{kind=link}

{kind=link}

Last update:

Oct 16, 2024