Theta 模型¶

Assimakopoulos & Nikolopoulos (2000) 的 Theta 模型是一种简单的预测方法,涉及拟合两条 \(\theta\)-线,使用简单指数平滑法对这两条线进行预测,然后将两条线的预测结果结合起来,生成最终的预测。该模型的实现步骤如下:

测试季节性

如果检测到季节性,则进行去季节化处理

通过将SES模型拟合到数据来估计\(\alpha\),并通过OLS估计\(b_0\)。

预测序列

如果数据已经去季节性化,请重新季节性化。

季节性检验检查季节性滞后 \(m\) 处的自相关函数(ACF)。如果该滞后显著不同于零,则使用 statsmodels.tsa.seasonal_decompose 对数据进行去季节化处理,使用乘法方法(默认)或加法方法。

模型的参数是 \(b_0\) 和 \(\alpha\),其中 \(b_0\) 是从OLS回归中估计出来的

并且 \(\alpha\) 是 SES 平滑参数

预测结果如下

最终,\(\theta\) 仅在确定趋势被抑制的程度时起作用。如果 \(\theta\) 非常大,那么模型的预测与带有漂移的积分移动平均值的预测相同。

最后,如果需要,预测结果会被重新季节性调整。

此模块基于:

Assimakopoulos, V., & Nikolopoulos, K. (2000). The theta 模型:一种分解预测方法。国际预测杂志, 16(4), 521-530.

Hyndman, R. J., & Billah, B. (2003). 揭开Theta方法的面纱。国际预测杂志, 19(2), 287-290.

Fioruci, J. A., Pellegrini, T. R., Louzada, F., & Petropoulos, F. (2015). 优化的theta方法。arXiv预印本 arXiv:1503.03529。

导入¶

我们从标准的导入集开始,并对默认的matplotlib样式进行一些调整。

[1]:

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pandas_datareader as pdr

import seaborn as sns

plt.rc("figure", figsize=(16, 8))

plt.rc("font", size=15)

plt.rc("lines", linewidth=3)

sns.set_style("darkgrid")

加载一些数据¶

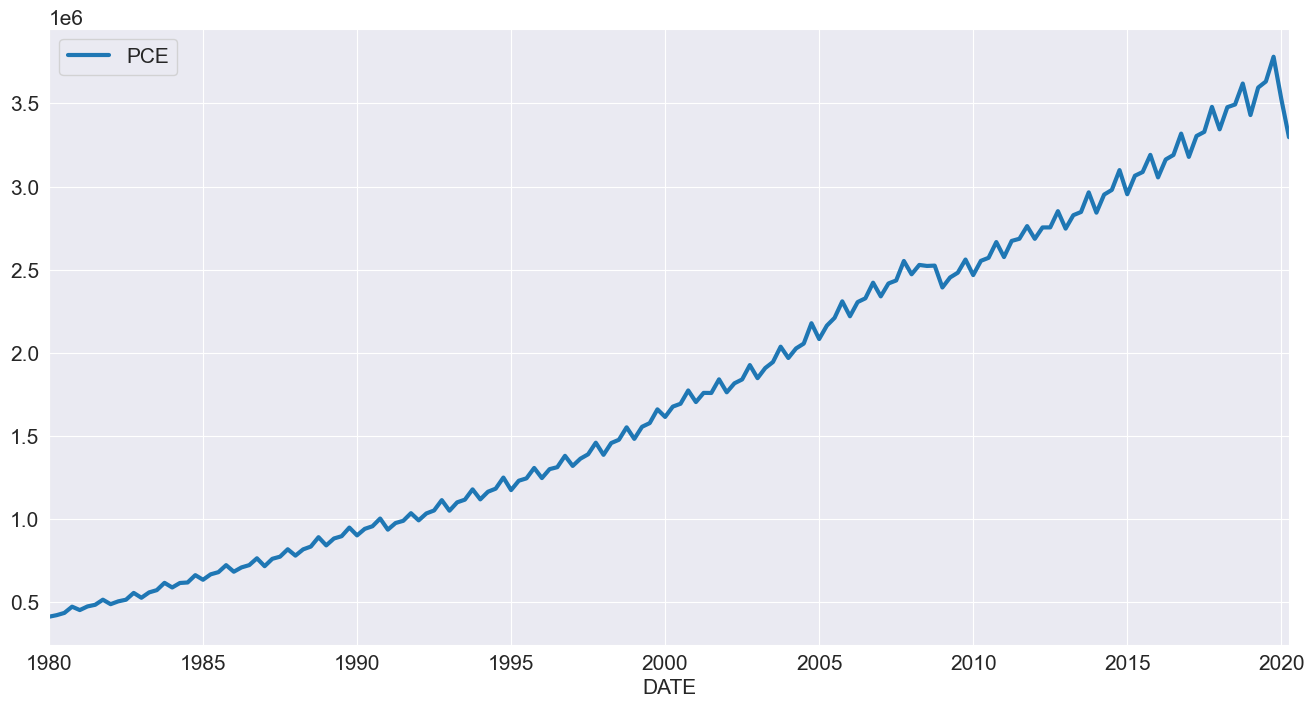

我们将首先使用美国数据来观察房屋开工情况。这一系列数据显然具有季节性,但在同一时期内并没有明显的趋势。

[2]:

reader = pdr.fred.FredReader(["HOUST"], start="1980-01-01", end="2020-04-01")

data = reader.read()

housing = data.HOUST

housing.index.freq = housing.index.inferred_freq

ax = housing.plot()

我们拟合了没有任何选项的模型并进行了拟合。摘要显示数据使用了乘法方法进行了去季节化处理。漂移是适度的且为负值,平滑参数相当低。

[3]:

from statsmodels.tsa.forecasting.theta import ThetaModel

tm = ThetaModel(housing)

res = tm.fit()

print(res.summary())

ThetaModel Results

==============================================================================

Dep. Variable: HOUST No. Observations: 484

Method: OLS/SES Deseasonalized: True

Date: Wed, 16 Oct 2024 Deseas. Method: Multiplicative

Time: 18:27:39 Period: 12

Sample: 01-01-1980

- 04-01-2020

Parameter Estimates

=========================

Parameters

-------------------------

b0 -0.9194460961668148

alpha 0.616996789006705

-------------------------

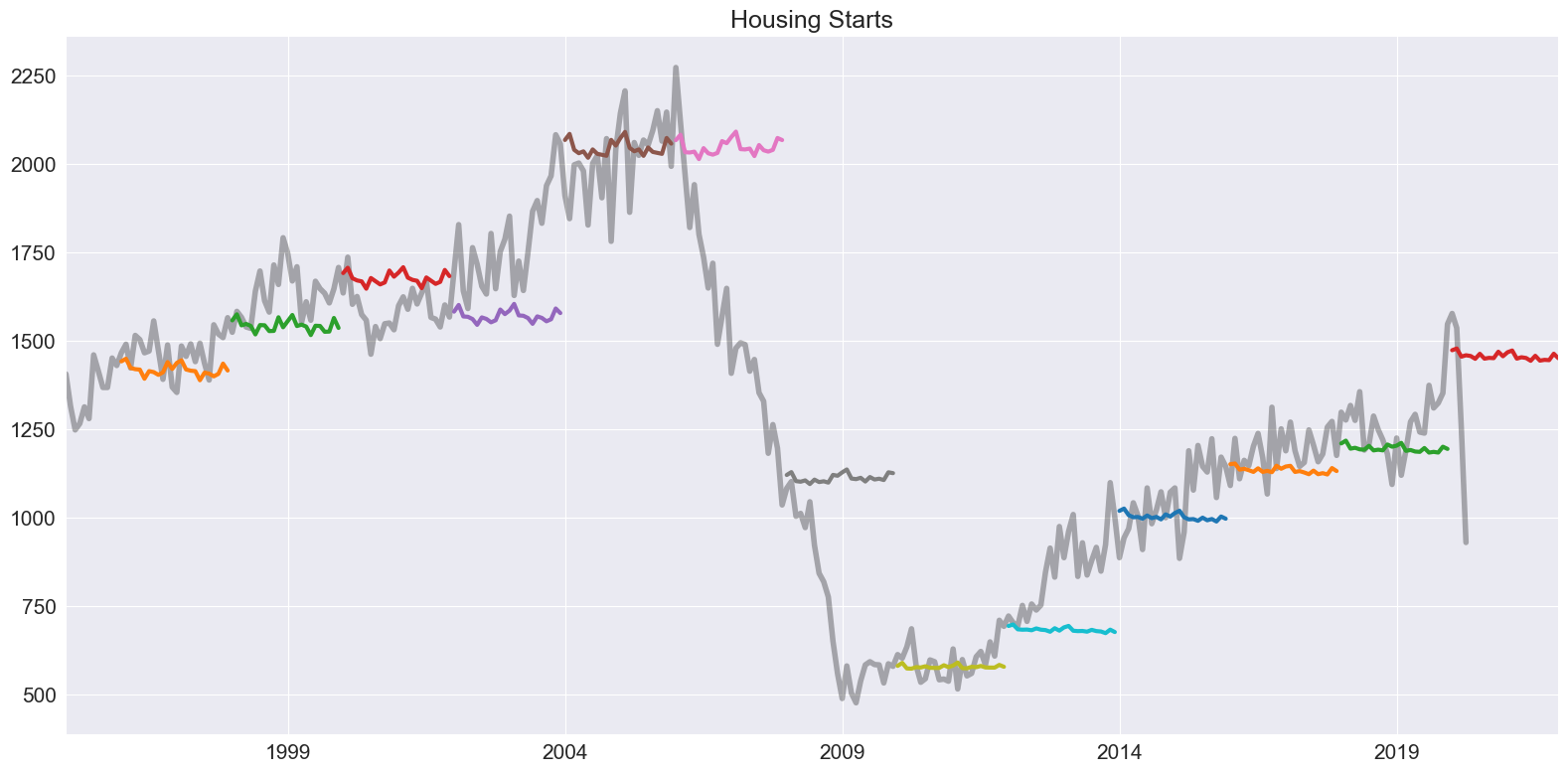

该模型首先是一种预测方法。使用拟合模型中的 forecast 方法生成预测。下面我们通过每两年预测未来两年生成一个刺猬图。

注意:默认的 \(\theta\) 是 2。

[4]:

forecasts = {"housing": housing}

for year in range(1995, 2020, 2):

sub = housing[: str(year)]

res = ThetaModel(sub).fit()

fcast = res.forecast(24)

forecasts[str(year)] = fcast

forecasts = pd.DataFrame(forecasts)

ax = forecasts["1995":].plot(legend=False)

children = ax.get_children()

children[0].set_linewidth(4)

children[0].set_alpha(0.3)

children[0].set_color("#000000")

ax.set_title("Housing Starts")

plt.tight_layout(pad=1.0)

我们可以选择拟合数据的自然对数。在这里,如果需要,强制使用加法方法进行去季节化更有意义。我们还使用最大似然估计(MLE)来拟合模型参数。这种方法拟合IMA

其中 \(\hat{\alpha}\) = \(\min(\hat{\gamma}+1, 0.9998)\) 使用 statsmodels.tsa.SARIMAX。参数相似,尽管漂移更接近于零。

[5]:

tm = ThetaModel(np.log(housing), method="additive")

res = tm.fit(use_mle=True)

print(res.summary())

ThetaModel Results

==============================================================================

Dep. Variable: HOUST No. Observations: 484

Method: MLE Deseasonalized: True

Date: Wed, 16 Oct 2024 Deseas. Method: Additive

Time: 18:27:40 Period: 12

Sample: 01-01-1980

- 04-01-2020

Parameter Estimates

=============================

Parameters

-----------------------------

b0 -0.00044644118699158845

alpha 0.6706103849698464

-----------------------------

预测仅取决于预测趋势成分,

来自SES的预测(不随时间范围变化),以及季节性。这三个组成部分可以通过forecast_components获得。这使得可以使用上述权重表达式,通过多种\(\theta\)选择来构建预测。

[6]:

res.forecast_components(12)

[6]:

| trend | ses | seasonal | |

|---|---|---|---|

| 2020-05-01 | -0.000666 | 6.95726 | -0.001252 |

| 2020-06-01 | -0.001112 | 6.95726 | -0.006891 |

| 2020-07-01 | -0.001559 | 6.95726 | 0.002992 |

| 2020-08-01 | -0.002005 | 6.95726 | -0.003817 |

| 2020-09-01 | -0.002451 | 6.95726 | -0.003902 |

| 2020-10-01 | -0.002898 | 6.95726 | -0.003981 |

| 2020-11-01 | -0.003344 | 6.95726 | 0.008536 |

| 2020-12-01 | -0.003791 | 6.95726 | -0.000714 |

| 2021-01-01 | -0.004237 | 6.95726 | 0.005239 |

| 2021-02-01 | -0.004684 | 6.95726 | 0.009943 |

| 2021-03-01 | -0.005130 | 6.95726 | -0.004535 |

| 2021-04-01 | -0.005577 | 6.95726 | -0.001619 |

个人消费支出¶

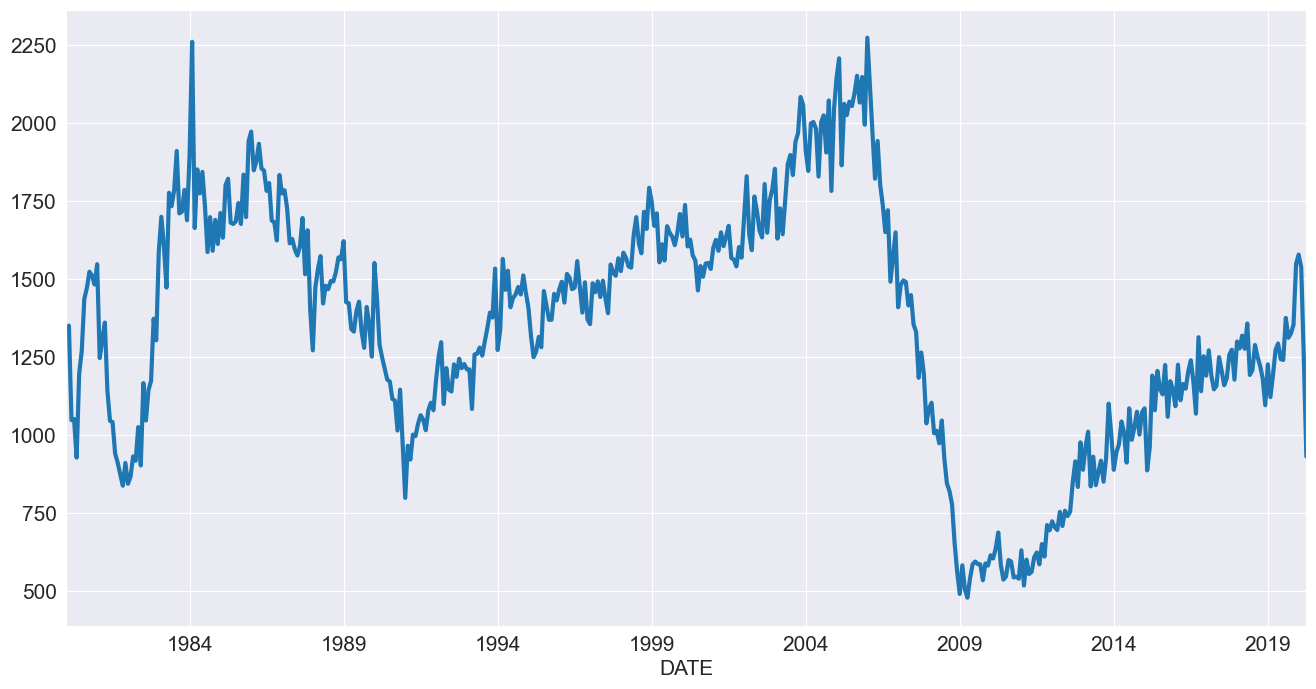

我们接下来考察个人消费支出。这一系列数据具有明显的季节性成分和趋势。

[7]:

reader = pdr.fred.FredReader(["NA000349Q"], start="1980-01-01", end="2020-04-01")

pce = reader.read()

pce.columns = ["PCE"]

pce.index.freq = "QS-OCT"

_ = pce.plot()

由于这个序列总是正的,我们对该序列进行\(\ln\)建模。

[8]:

mod = ThetaModel(np.log(pce))

res = mod.fit()

print(res.summary())

ThetaModel Results

==============================================================================

Dep. Variable: PCE No. Observations: 162

Method: OLS/SES Deseasonalized: True

Date: Wed, 16 Oct 2024 Deseas. Method: Multiplicative

Time: 18:27:42 Period: 4

Sample: 01-01-1980

- 04-01-2020

Parameter Estimates

==========================

Parameters

--------------------------

b0 0.013035370221488499

alpha 0.9998851279204637

--------------------------

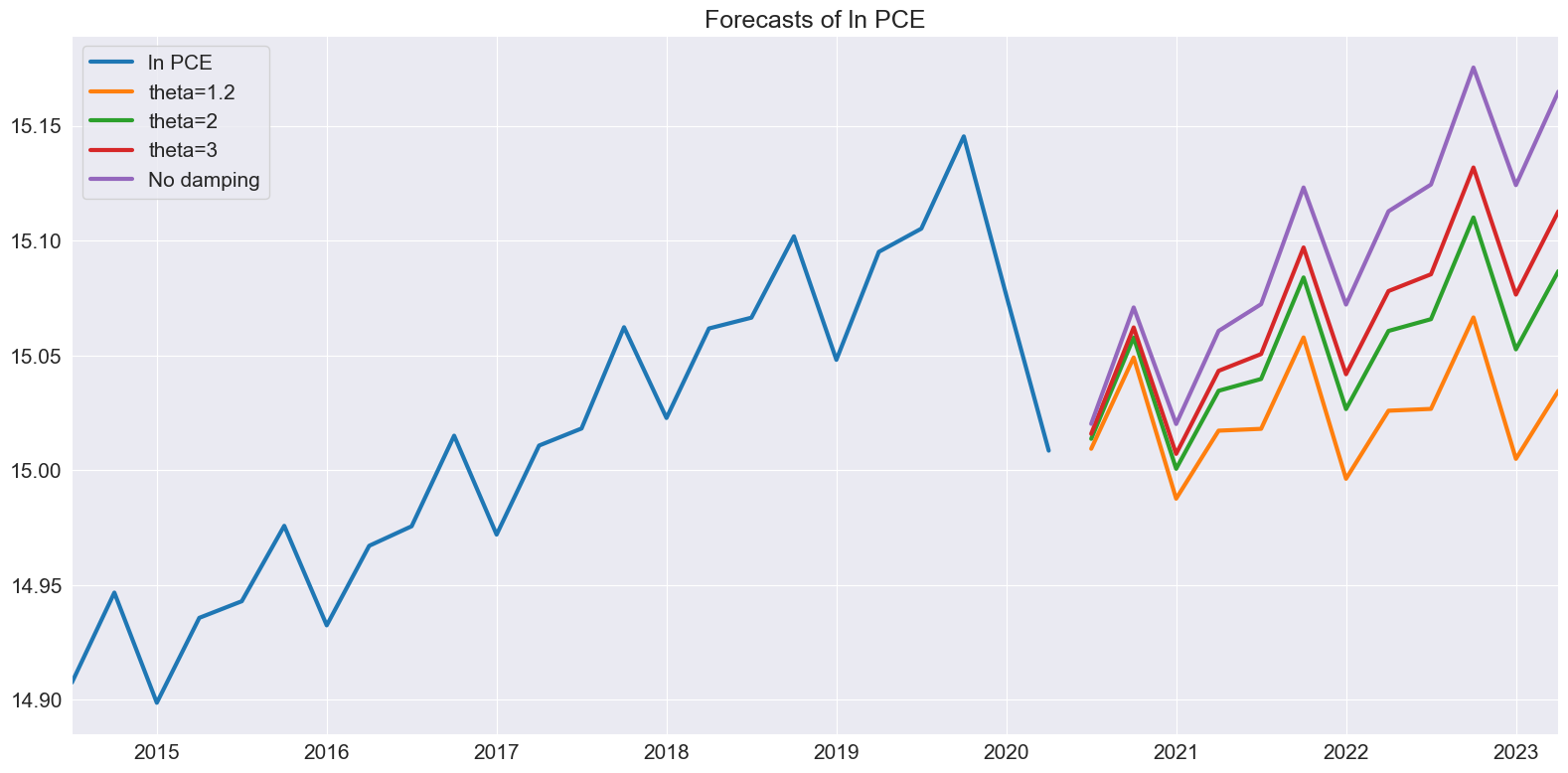

接下来我们探讨随着 \(\theta\) 的变化,预测中的差异。当 \(\theta\) 接近1时,漂移几乎不存在。随着 \(\theta\) 的增加,漂移变得更加明显。

[9]:

forecasts = pd.DataFrame(

{

"ln PCE": np.log(pce.PCE),

"theta=1.2": res.forecast(12, theta=1.2),

"theta=2": res.forecast(12),

"theta=3": res.forecast(12, theta=3),

"No damping": res.forecast(12, theta=np.inf),

}

)

_ = forecasts.tail(36).plot()

plt.title("Forecasts of ln PCE")

plt.tight_layout(pad=1.0)

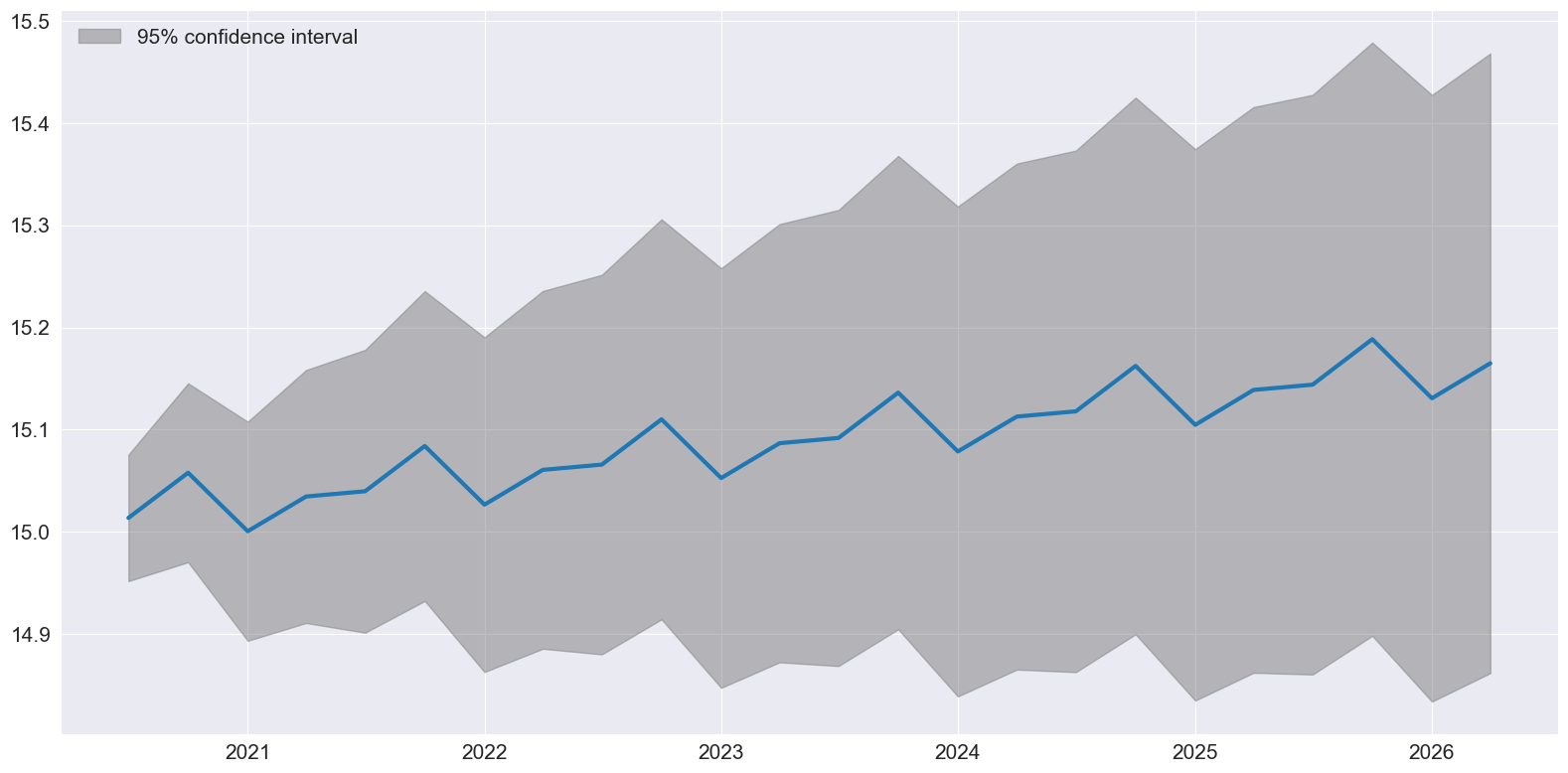

最后,plot_predict 可以用于可视化预测和预测区间,这些预测和预测区间是假设IMA为真的情况下构建的。

[10]:

ax = res.plot_predict(24, theta=2)

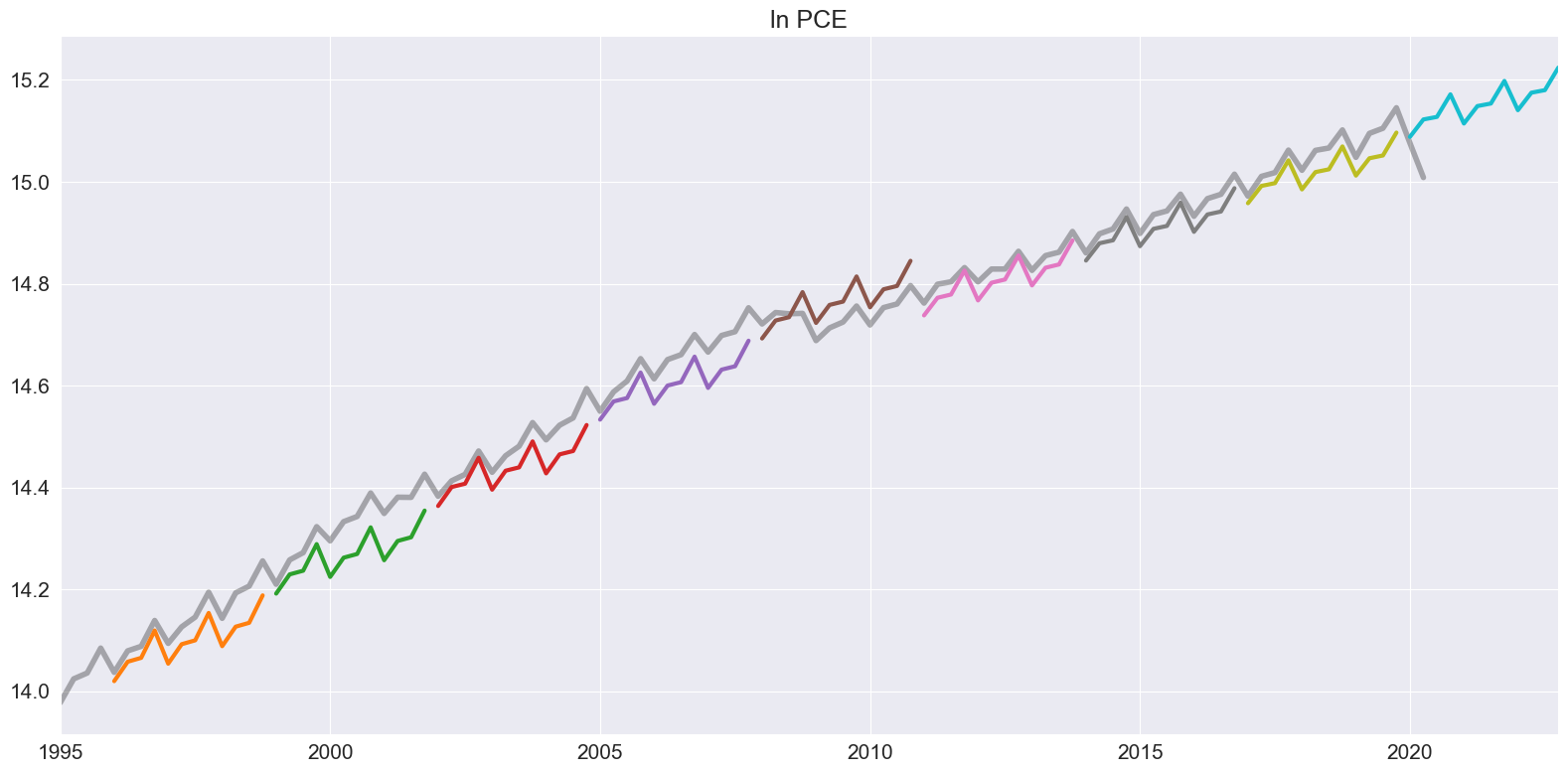

我们通过使用2年非重叠样本来生成刺猬图。

[11]:

ln_pce = np.log(pce.PCE)

forecasts = {"ln PCE": ln_pce}

for year in range(1995, 2020, 3):

sub = ln_pce[: str(year)]

res = ThetaModel(sub).fit()

fcast = res.forecast(12)

forecasts[str(year)] = fcast

forecasts = pd.DataFrame(forecasts)

ax = forecasts["1995":].plot(legend=False)

children = ax.get_children()

children[0].set_linewidth(4)

children[0].set_alpha(0.3)

children[0].set_color("#000000")

ax.set_title("ln PCE")

plt.tight_layout(pad=1.0)